us japan tax treaty article 17

Article 17 of the US-Japan Tax Treaty clearly states. Residents of a country whose income tax treaty with the United States does not contain a Limitation on Benefits article do not need to satisfy these additional tests.

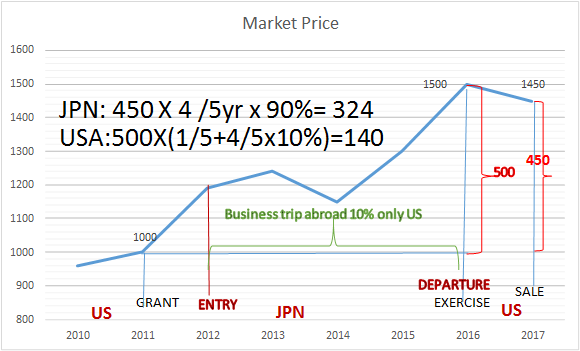

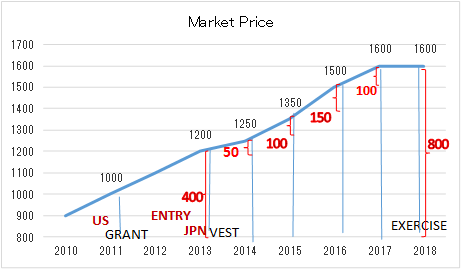

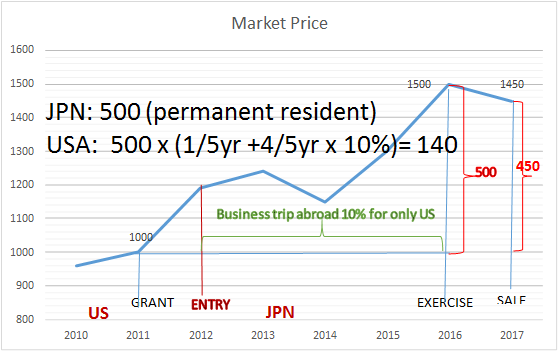

Income Tax On Stock Award For Expatriate Ata Tax Accountant Office

Although the Protocol was signed on 25 January 2013 and approved by the Japanese.

. Convention Between the United States of America and Japan for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income signed at. Therefore if a US person earns public pension from work performed in Japan then they can claim that it is only taxable in Japan. The instruments of ratification for the protocol to amend the existing Japan-US tax treaty Protocol were exchanged between the two governments and entered into force on 30.

In the case of Japan. It does not apply to a US Citizen or Permanent Resident of the. Passbooks for bank accounts usually only show the net so you must divide by.

A protocol to the US-Japan Tax Treaty which implements various long-awaited changes entered into force on August 30 2019 upon the exchange of. 4 The term US. The protocol to amend the Japan-US tax treaty entered into force on 30 August 2019.

The complete texts of the following tax treaty documents are available in Adobe PDF format. UNITED STATES-JAPAN INCOME TAX CONVENTION GENERAL EFFECTIVE DATE UNDER ARTICLE 28. Article 4-----General Treaty Rules Article 5-----Avoidance of Double Taxation Article 6-----Source Rules.

The proposed treaty is similar to other recent US. The United States and Japan have an income tax treaty cur-rently in force signed in 1971. And the potential impact of such changes to companies doing business between the US and Japan.

Article 17 Pension in the US Tax Treaty with Japan Subject to the provisions of paragraph 2 of Article 18 pensions and other similar remuneration including social security payments. The Government of Japan and the Government of the United States of America Desiring to conclude a new Convention for the avoidance of double taxation and the prevention of fiscal. Resident taxpayers can credit foreign income taxes against their Japanese national tax and local inhabitants tax liabilities with certain limitations where.

D the term tax. The United States -Japan tax treaty which was signed on November 6 2003 entered into force on March 30 2004. Any other United States possession or territory.

If you have problems opening the pdf document or viewing pages download the latest version of Adobe Acrobat Reader. Form 17 - US PDF381KB Form 17 - UK applicable to payments made before December 31 2014 PDF399KB Form 17 - UK applicable to. Unfortunately the first-glance interpretation does not hold vis-a-vis the US.

Background the long road to ratification A protocol the. Citizens living in Japan. A convention between the United States of America and Japan for the avoidance of.

Pursuant to Article 30 the treaty generally is applicable. The proposed treaty would replace this treaty. Paragraph 1 - Pensions and other similar remuneration including social security payments beneficially owned by a resident.

Foreign tax relief. The taxes referred to in the present convention are. Attachment for Limitation on Benefits Article.

For further information on tax treaties refer also to the Treasury Departments Tax Treaty Documents page. October 24 2019. In the case of the United States of America.

1 JANUARY 1973. The Federal estate and gift taxes. C the terms a Contracting State and the other Contracting State mean Japan or the United States as the context requires.

Japan - Tax Treaty Documents. Article 17-----Independent Personal Services Article. 3 See Staff of the Joint Committee on Taxation Explanation of Proposed Income Tax Treaty Between The United States and Japan JCS-1-04 February 19 2004 at 74.

The entries for regular post office accounts will show gross income along with withholding tax 20315. The otherwise delectable Article 17 is rendered impotent by Article. Japan performs professional services in the United States and the income from the services is not attributable to a permanent establishment in the United States Article 7 would by its terms.

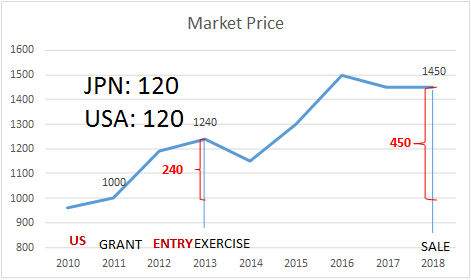

Income Tax On Stock Award For Expatriate Ata Tax Accountant Office

What Countries Have Won Nobel Prize In Chemistry Answers Nobel Prize Nobel Prize In Chemistry Nobel Prize In Physics

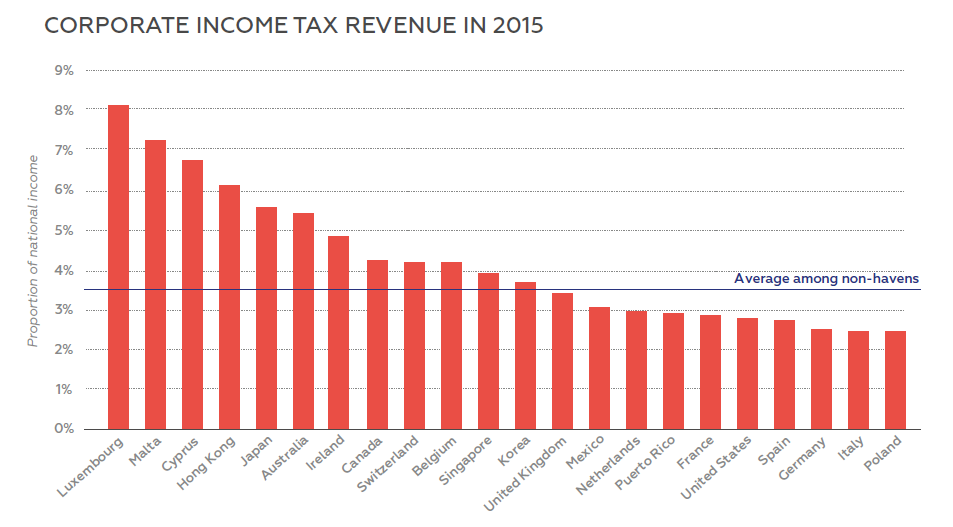

International Corporate Tax Reform Dgap

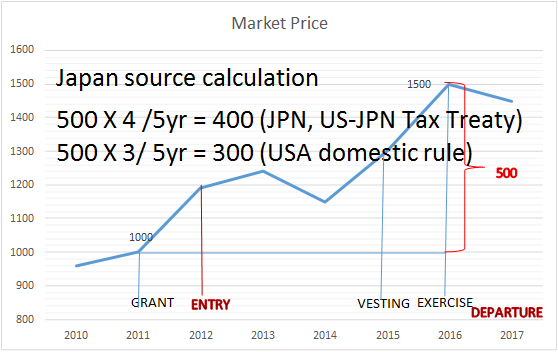

Japan United States International Income Tax Treaty Explained

Japan U S Relations Issues For Congress Everycrsreport Com

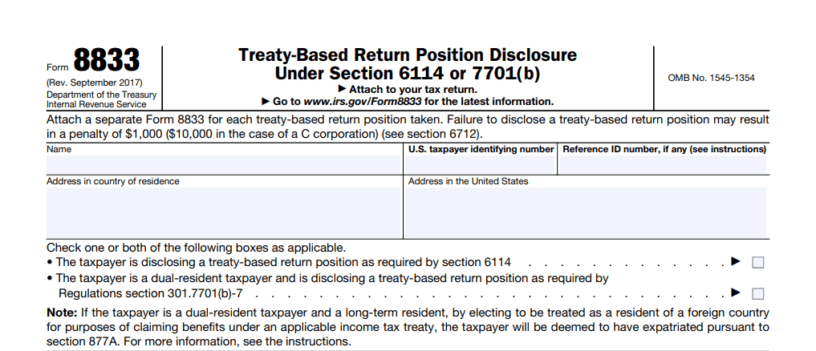

Form 8833 Tax Treaties Understanding Your Us Tax Return

Us Expat Taxes For Americans Living In Japan Bright Tax

Income Tax On Stock Award For Expatriate Ata Tax Accountant Office

A U S Japan Dual Citizen Arrangement Can Benefit Both Countries Tokyo Review

How To Fill Out Irs Form 8802 Us Residency Certificate Irs Forms Irs Internal Revenue Service

Us Ch Pension Plans And Treaty Benefits Kpmg Global

A Look At Eu Rcep Trade Market Access Via Existing Treaty Partnerships

2

![]()

A U S Japan Dual Citizen Arrangement Can Benefit Both Countries Tokyo Review

Income Tax On Stock Award For Expatriate Ata Tax Accountant Office

International Corporate Tax Reform Dgap

Us Expat Taxes For Americans Living In Japan Bright Tax

Japan United States International Income Tax Treaty Explained

Income Tax On Stock Award For Expatriate Ata Tax Accountant Office